EV Switching Signals in East Asia: How Consumer Sentiment Varies Across Japan, South Korea, and China

2026/03/16

Table of Contents

Background of Study

Electric Vehicles (EV) adoption in East Asia is far from uniform. Even among geographically close markets—Japan, South Korea, and China—consumers’ willingness to shift to EVs, and the ease of living with one, can differ sharply.

Leveraging GMO Research & AI’s automotive panel, a study was conducted in January 2026 to examine switching tendencies for the next private vehicle purchase. This article then unpacks what drives these gaps: general car purchase priorities, fuel-type reasons for choosing EVs versus hybrid vehicles, and practical barriers such as charging readiness and dependence on policy incentives.

Survey Specifications

Survey Date: 23-30 January 2026

Method: Online survey

Target Group: Private car owners in Japan, South Korea, China

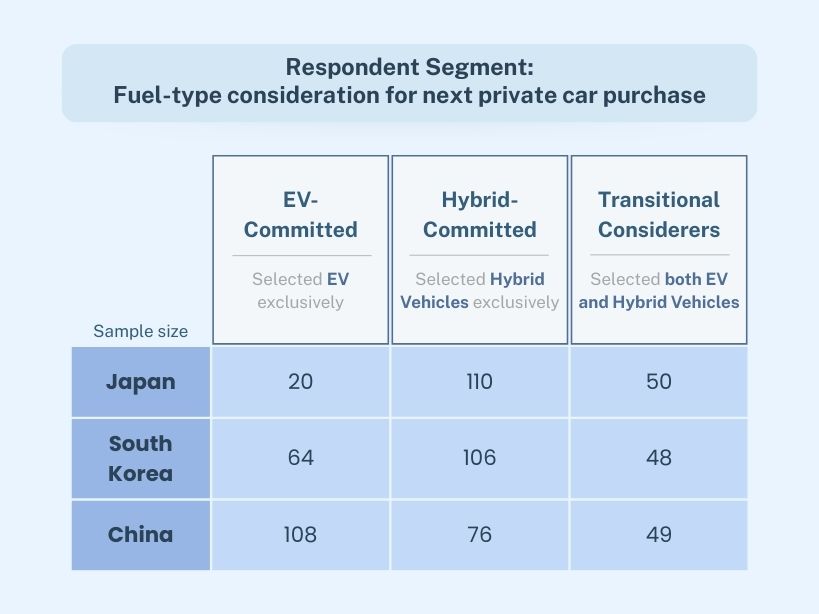

Sample size: 419ss in Japan/ 311ss in South Korea/ 328ss in China

Conducted by: GMO Research & AI

|

For online research in Asia, learn how GMO Research & AI's online panel supports your needs. |

Respondent Segment Definition

Respondents were segmented according to their stated fuel-type consideration for their next private car purchase (multiple response format). Based on selection patterns, three mutually exclusive analytical groups were constructed to distinguish consumers who have already made a clear directional choice from those who remain open to both technologies.

- EV-Committed: Respondents selecting battery electric vehicles exclusively.

- Hybrid-Committed: Respondents selecting hybrid vehicles exclusively.

- Transitional Considerers: Respondents selecting both EV and hybrid options.

*Click to expand image

Are Non-EV Owners in East Asia Switching to EV?

This section examines switching signals by comparing current fuel-type ownership with next purchase intention.

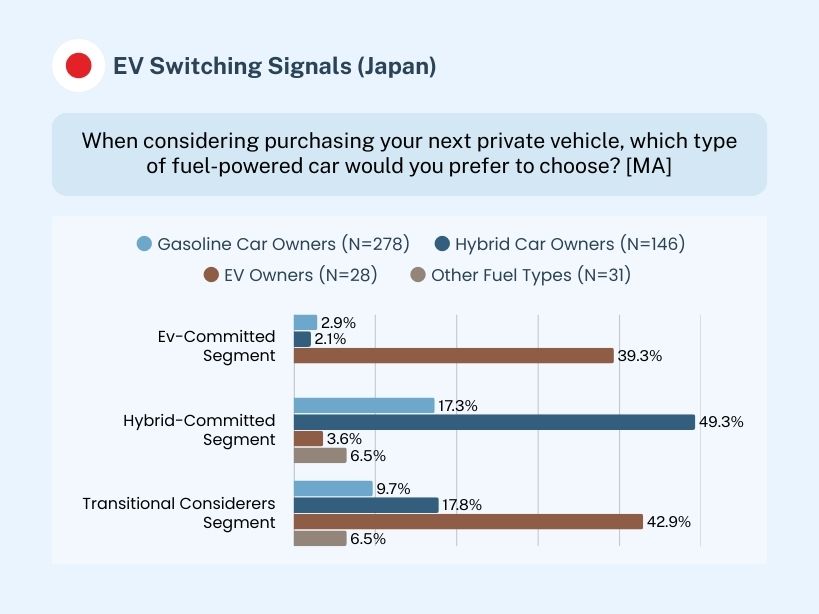

Japan — Hybrid-Centered Stability

Switching intentions from gasoline or hybrid vehicles to exclusively EVs remain limited, reflecting a cautious switching environment, with hybrid vehicles continuing to function as the dominant transition anchor.

- Hybrid vehicle owners (N= 146): 49.3% remain Hybrid-Committed, while only 2.1% indicate EV-only consideration. An additional 17.8% fall into the Dual segment.

- Gasoline vehicle owners (N= 278): only 2.9% express exclusive EV commitment. Hybrid vehicles remain more attractive with 17.3%, while 9.7% consider both options.

- Current EV owners (N= 28): loyalty is not absolute. While 39.3% remain EV-Committed, 42.9% consider both EV and hybrid, and 3.6% indicate exclusive hybrid consideration.

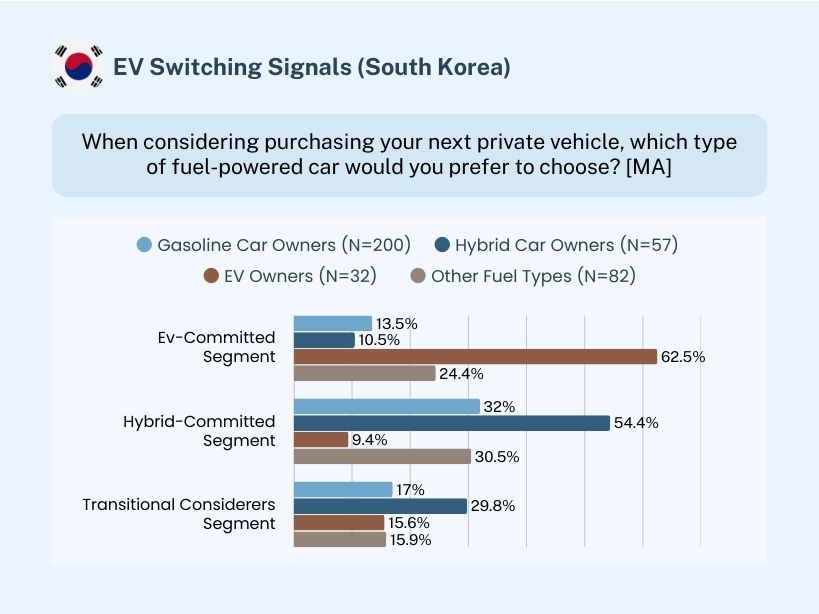

South Korea — Competitive Dual-Path Switching

EV switching signals are more visible than in Japan but hybrid vehicles still retain stronger pull among non-EV owners.

- Hybrid vehicle owners (N= 57): 54.4% remain Hybrid-Committed, while 10.5% express EV-only intention.

- Gasoline vehicle owners (N= 200): 13.5% are EV-Committed, compared with 32% Hybrid-Committed, and 17% Dual.

- Current EV owners (N= 32): loyalty is strong with 62.5% remaining EV-Committed, while only 9.4% consider hybrid exclusively.

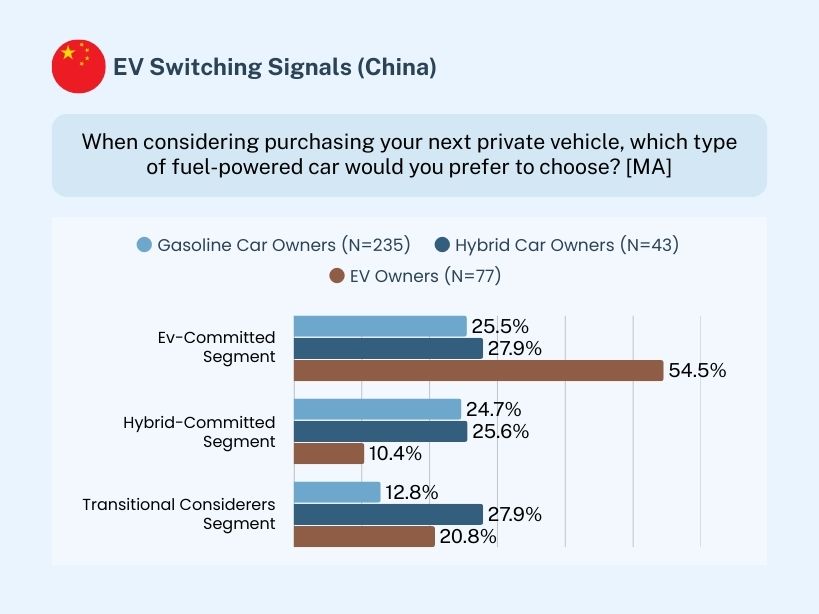

China — Direct EV Migration Signals Emerging

More balanced switching signals between EV and hybrid vehicles are observed in China. The ownership–intention pattern indicates active movement across fuel types, with EV positioned as a viable next-step option for multiple ownership bases.

- Hybrid vehicle owners (N= 43): 27.9% select EV exclusively, equal to those considering both, while 25.6% remain hybrid-only.

- Gasoline vehicle owners (N= 235): 25.5% select EV exclusively, compared with 24.7% for hybrid, and 12.8% Dual.

- Current EV owners (N= 77): 54.5% remain EV-Committed, while 10.4% consider hybrid exclusively and 20.8% consider both.

Motivations and Barriers for EV-Purchasing

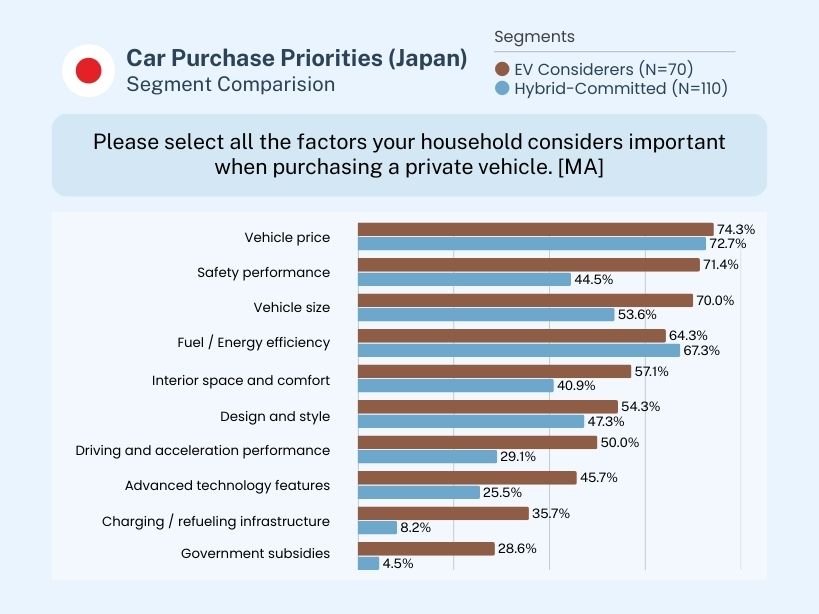

Japan — Pragmatic Baseline with Conditional EV Appeal

The Japanese market currently exhibits a greater propensity for hybrid vehicles. Although government incentives are in place, the selection of electric vehicles available in the market remains constrained, and the charging infrastructure is still inadequate.

*Transitional Considerers are analyzed together with EV-Committed respondents as an EV Considerers group.

The market context aligns with the survey results. General car purchase priorities remain firmly pragmatic for both Hybrid-only and EV Considerers. Vehicle price is prioritized at a similar level (72.7% vs. 74.3%), as is fuel/energy efficiency (67.3% vs. 64.3%).

EV Considerers place substantially higher importance on charging infrastructure availability (35.7% vs. 8.2%) and government incentives (28.6% vs. 4.5%), indicating that “practical readiness” is a decisive filter for EV consideration. They also show a more technology- and performance-oriented layer of interest, such as acceleration performance (50% vs. 29.1%) and advanced technology features (45.7% vs. 25.5%), but remain secondary to cost fundamentals.

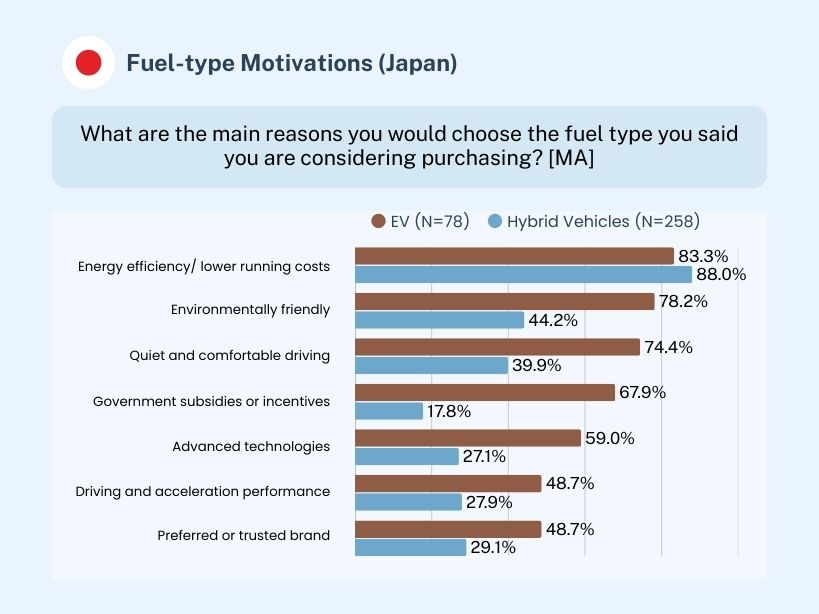

Fuel-type motivations show a similar structure where economic logic remains central. Fuel/energy efficiency is the leading justification for choosing both hybrid vehicles (88%) and EV (83.3%). EV differentiates through added-value motivations—environmentally friendly (78.2% vs. 44.2%), quiet and comfortable driving (74.4% vs. 39.9%), government incentives (67.9% vs. 17.8%), and advanced technology (59% vs 27.1%).

Taken together, while advanced technology and performance are also attractive elements for EV consideration, it may not fully align with mainstream cost-oriented and practical decision standards like hybrid vehicles, due to infrastructure and supply constraints of the market.

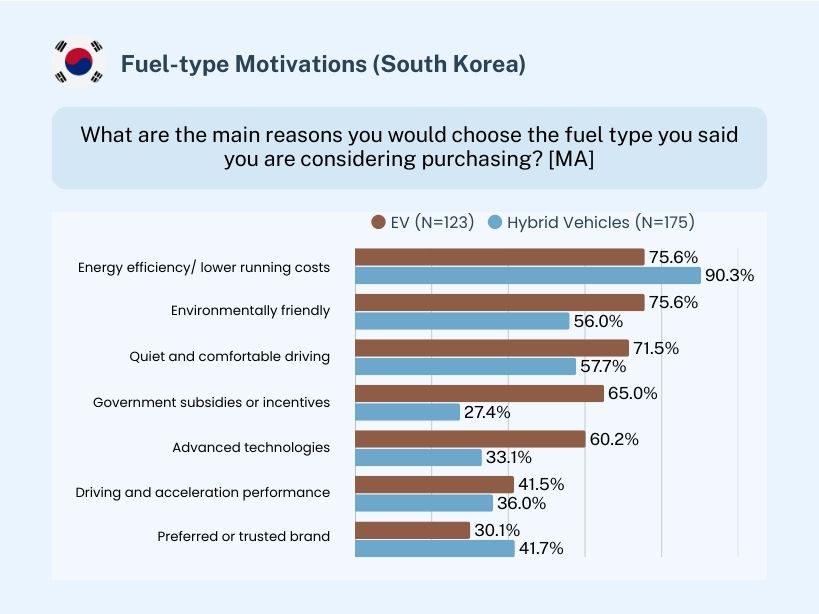

South Korea — Practical Baseline with Competitive EV Differentiation

In South Korea, hybrid vehicles remain strong, while EV registrations are growing alongside policy support and charging expansion—yet charging convenience is still cited as a barrier.

According to the survey result, general car purchase priorities show a stable “baseline first” logic of vehicle price (68.8%–77%), fuel/ energy efficiency (62.5–75%), and safety (57.8–68.8%) across segments. The decisive differences appear mainly among Transitional Considerers, who require proof on ownership practicality—driving/acceleration performance (50% vs. 29% in other groups), after-sales/dealer network (45.8% vs. 18.8%-27.4%), and charging infrastructure (37.5% vs. 22.6%-26.6%).

Fuel-type motivations reinforce Korea’s “baseline + added value” structure. Hybrid vehicles are strongly anchored by fuel efficiency (90.3%). EV is also supported by fuel efficiency (75.6%), but differentiates via environmentally friendliness (75.6% vs. 56%), government incentives (65% vs. 27.4%), advanced technology (60.2% vs. 33.1%), and quiet and comfortable driving (71.5% vs. 57.7%).

Overall, while EV has already established an innovative image, and interest towards the technology is observable, broader adoption depends on confidence in ownership support and charging practicality.

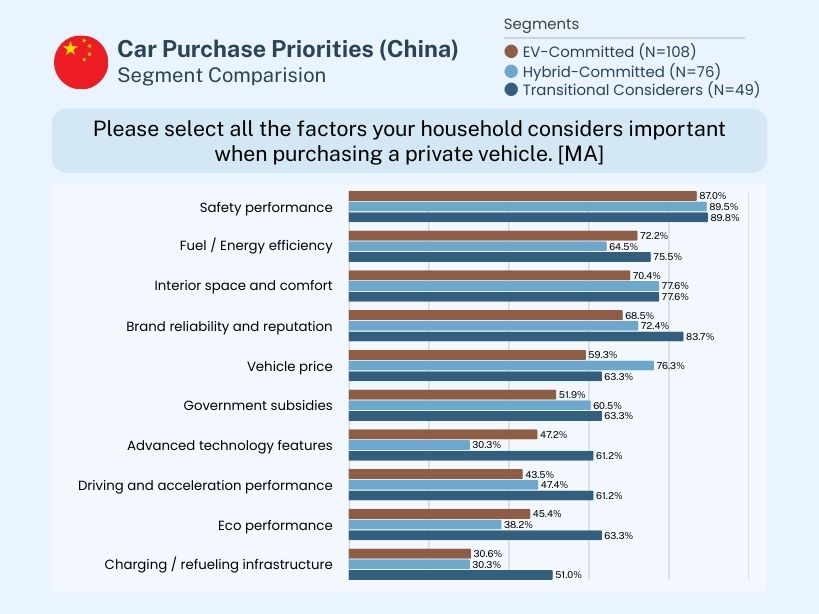

China — Mainstream Integration and Reduced Switching Friction

China’s EV transition is supported by a mature ecosystem, including the world’s largest public charging network serving the world’s largest EV fleet. Government policy support also remains a tailwind, with purchase-tax incentives extended through end-2027 .

Survey results reflect car purchase priorities highly emphasized on safety (87–89.8%), brand reputation (68.5–83.7%), interior space/comfort (70.4–77.6%), and energy efficiency (64.5–75.5%). The mainstream evaluation set blends brand and comfort expectations, supported with economic considerations.

Within this, the EV-Committed segment is more technology-forward (advanced tech 47% vs. hybrid 30%), while Hybrid-Committed lean more to price (76.3%) and after-sales networks (51%). Transitional Considerers presents significant gaps surrounding driving/acceleration performance (61.2%), eco performance (63.3%), and charging infrastructure (51%), showing “EV tech value + readiness check” in parallel.

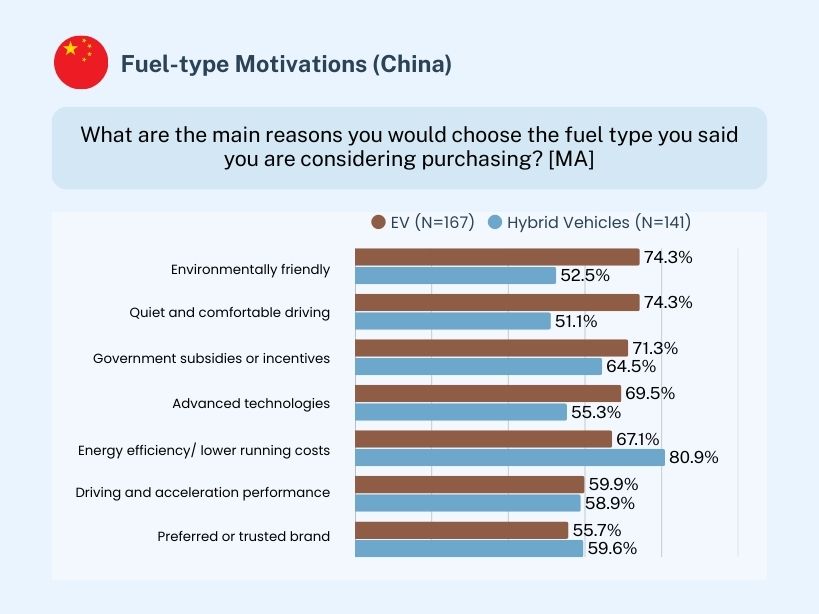

Fuel-type motivations are consistent with general car purchase priority. Government incentives are high for both hybrid vehicles (64.5%) and EV (71.3%). EV still differentiates via environmentally friendliness (74.3% vs. 52.5%), quiet and comfortable driving (74.3% vs. 51.1%), and advanced technology (69.5% vs. 55.3%). Crucially, brand reliability is selected not only for hybrid vehicles(59.6%) but also for EVs (55.7%), suggesting EV is not treated as a “risk trade-off” for technology-oriented values, but as compatible with mainstream trust cues.

Market-by-Market Evidence Matters

EV adoption in East Asia cannot be treated as a single regional story. Japan, South Korea, and China sit at different points on the transition curve, shaped by distinct market realities—from model availability and charging readiness to incentives and the way consumers weigh risk versus added value. This underscores the critical need to consider regional variations when designing international research and analyzing survey data. GMO Research and AI remains dedicated to sharing Asia-related insights and is prepared to support your research needs throughout the region.

For a full picture and detailed survey results,

please feel free to download the tabulated data.

Looking for more insights for the Asian Automotive market?

Find out more from our previous studies!

|

Reviewed by: Yukiya Nagata

Executive Managing Director of GMO Research & AI

|

Joined GMO Research & AI in 2011, Yukiya was the domestic sales director of the Japan headquarter until 2016. He then shifted to a new role of managing the global panel and developed online research services in South-East Asia. He also launched the Malaysia office, operating the company as a managing director until 2021. As a board member, his current role involves seeking new business opportunities and partners worldwide.